Congratulations for being retired or having enough money to never work again! Don’t listen to the naysayers who tell you retirement life is boring. Be assured that only boring people get bored. One question you should consider thinking about, however, is exactly how much investment risk should you be taking.

Congratulations for being retired or having enough money to never work again! Don’t listen to the naysayers who tell you retirement life is boring. Be assured that only boring people get bored. One question you should consider thinking about, however, is exactly how much investment risk should you be taking.

In 2012, I retired from the salt mines because I thought I had enough to provide a humble life for a family of up to four in San Francisco. But once I stopped receiving a bi-weekly paycheck, reality hit home that maybe my passive income and side hustle income wouldn’t be enough. The fact that I tried to sell my primary residence in 2012 to live in an apartment 65% smaller and cheaper shows that I had reservations about whether it was wise to leave a healthy paycheck at 34. But I was determined to provide a free life for my wife and I both before the age of 35.

In early retirement, I concluded that I needed to take the least amount of risk necessary to maximize my chances of never having to go back to work full-time again. At the same time, I was still pretty young and it looked like the economy was recovering so I ended up constructing a 60%-70% stock and 30% – 40% bond portfolio with the hopes of achieving a 4% – 6% rate of return each year. Doubling my investments by the age of 50 seemed like a good enough goal to have.

But thanks to a bull market in stocks and bonds, my public investment portfolio returned more. And thanks to a strong recovery in San Francisco real estate, everything has turned out fine so far. I wasn’t smart, I just stuck to an investment framework that fit my risk profile.

But I “Missed Out BIG TIME”

In 2017, my public investment portfolio returned 15.9%. Given my annual return objective was only 4% – 6%, I was feeling pretty good about the performance. Then of course a commenter left this lovely comment after reading my investment lessons from a surreal 2017 post. I wrote that due to uncertainty, I didn’t pile into stocks at the beginning of the year.

You missed out BIG TIME then. Seemed pretty obvious that the stock market would soar once Trump was elected despite what many so called experts said. Regardless of accomplishments, investors gained trust in the market again once a businessman was elected as opposed to another career politician (on either side).

Isn’t it interesting how all investment decisions are obvious in hindsight? Yes, my combined stock and bond portfolio underperformed the S&P 500 index by about 3.5%, but my stock only exposure outperformed since I was heavy in tech. I didn’t invest my entire portfolio in the stock market because I wasn’t comfortable with the risk.

For those of you who may feel bad about your investment performance or were criticized by others for not doing better let me share some following thought gems:

1) You’re already free. Money is a means to an end. If you’re able to earn or accumulate enough to be free to do whatever you want every day, you win. It’s much better to only be up 10% and do your own thing than be up 50%, but still have to report to someone.

2) Don’t forget the absolute dollar return. As someone who is close to retirement or in retirement, you’ve likely already got way more capital than someone who is still far away from retirement. Therefore, the absolute dollar amount you return is also much greater. It’s much better to be up $1 million on a 15.9% return than be up $100,000 on a 100% return.

3) Don’t forget all your other assets. You likely have a wide assortment of investments as part of your net worth compared to most Americans who have most of their net worth in their primary residence. Even if your public investments underperform, your other asset classes such as coastal city real estate, private equity, venture capital, real estate crowdfunding, venture debt, fine art, etc might outperform.

4) More money won’t make you happier. After you earn more than ~$100,000 a year in a non-coastal city or ~$300,000 a year in a coastal city, you won’t be happier. The same can be said with building a greater net worth beyond what you’ve deemed necessary to retire on. But if you want a specific net worth number, I will say anything above a $3 million net worth won’t make you much happier if you are truly free to do what you want and don’t have to make your partner work to enjoy your lifestyle.

5) It’s great to sleep well at night. All retirees know what it’s like to lose money because we’ve been through enough down cycles. When you can combine the freedom to do what you want with not having to worry about ever going to work because your investments are generating enough income, you feel like the luckiest person on Earth. Not only have you won the game, you get invited back as a VIP with front row seats and all you can drink and eat privileges.

Retirement Investment Risk Levels

Zero risk: Your baseline investment goal in retirement is to at least beat inflation. You can easily beat inflation with no risk if you invest all your money in treasury bonds. With inflation hovering around 2% a year and the 10-year bond yield providing a ~2.7% yield, you’re golden, forever. Treasuries will almost always yield more than inflation. So long as you hold your treasury bond until maturity, you will get all your principal back plus the annual coupon.

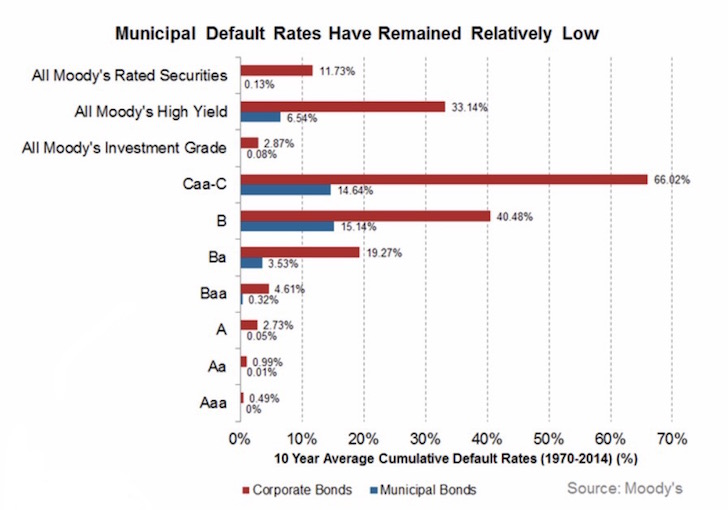

Minimal risk: The next investment you can make is to invest your entire liquid net worth in a portfolio of the highest rated municipal bonds in your state. You can find 20-year municipal bonds yielding 3.8% – 4% tax free. AAA-rated municipal bonds have default rates under 1%. In 15.5 years, you’ll double your money. So long as you hold your municipal bond until maturity, you will get all your principal back plus the annual coupon, if the municipality doesn’t go bankrupt.

Moderate risk: The Barclays U.S. Aggregate Bond Index provides about a 5% annual return each year, depending on which 10 year time frame you’re looking at. You can take more risk buying individual corporate bonds, emerging market bonds, or high yield bonds. But overall, buying the aggregate bond index is a moderately risky investment. If you buy an index fund, you have no guarantee of getting your principal back. You are riding appreciation or depreciation and collecting coupons. Corporations can default or corporate bonds can lose principal value if a corporation experiences financially difficulty. There are no guarantees. If you bought Venezuela sovereign bonds you’d be down big as the government is in disarray and inflation is sky high.

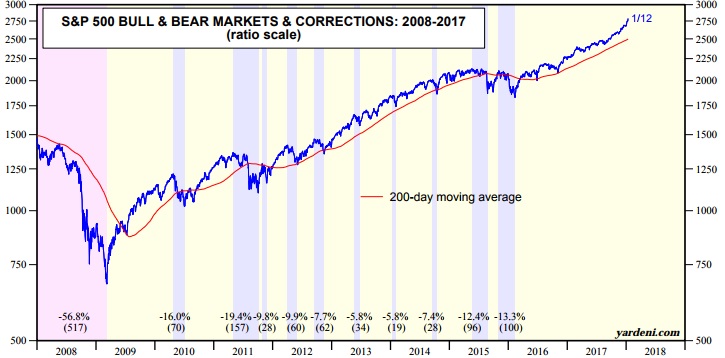

Higher risk: The stock market has returned anywhere from 8% – 10% a year on average, depending on the time frame you are looking at. Just like in the bond market, you can buy all sorts of different stocks with different risk profiles. But as we know, the stock market can have violent corrections. See the recent number and magnitude of corrections below in the chart.

Retirees will have a combination of different types of risk levels. The question to ask is what type of investment weightings one should have in each based on their risk profile.

There is no right answer because everybody’s risk tolerance is different. But we can start by looking at the risk / reward metrics of different types of portfolios.

Income Based Retirement Portfolio

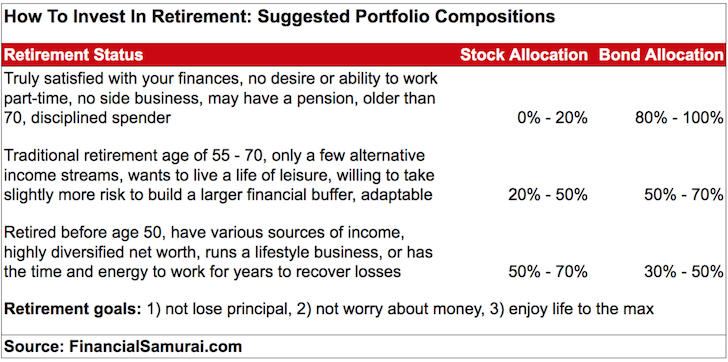

Income based portfolios are what the typical, truly satisfied retirees should focus on. There’s minimal risk to principal and only modest medium-to-long term growth of principal. Given retirees are generally in a lower tax bracket, an income based portfolio is also usually more tax efficient.

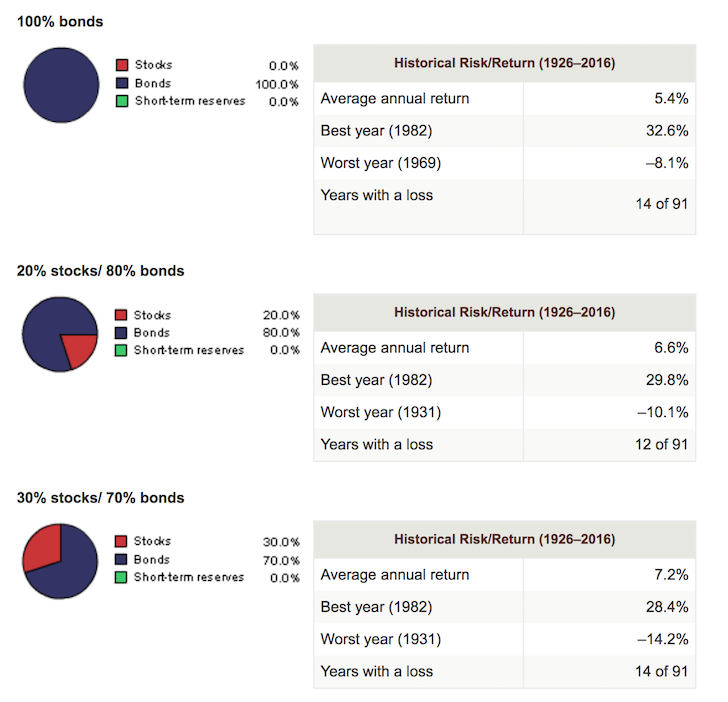

Even with a super conservative 100% allocation in bonds, your average annual return would be 5.4%, beating inflation by roughly 3.4% a year and twice the current risk free rate of return. In 14 years, your retirement portfolio will have doubled.

With a 30% allocation to stocks, you could improve your investment returns by 1.8% a year. But if you are already satisfied with the amount of money you have, who cares about an extra 1.8% a year? The improved performance will make no difference in your lifestyle. With a potential improvement of 1.8% a year, you increase the magnitude of a potential loss by 75% (from -8.1% to -14.2%) based on history.

Source: Vanguard

Balanced Retirement Portfolio

A balanced-oriented investor seeks to reduce potential volatility by including income-generating investments in his or her portfolio and accepting moderate growth of principal. This type of investor is also willing to tolerate short-term price fluctuations.

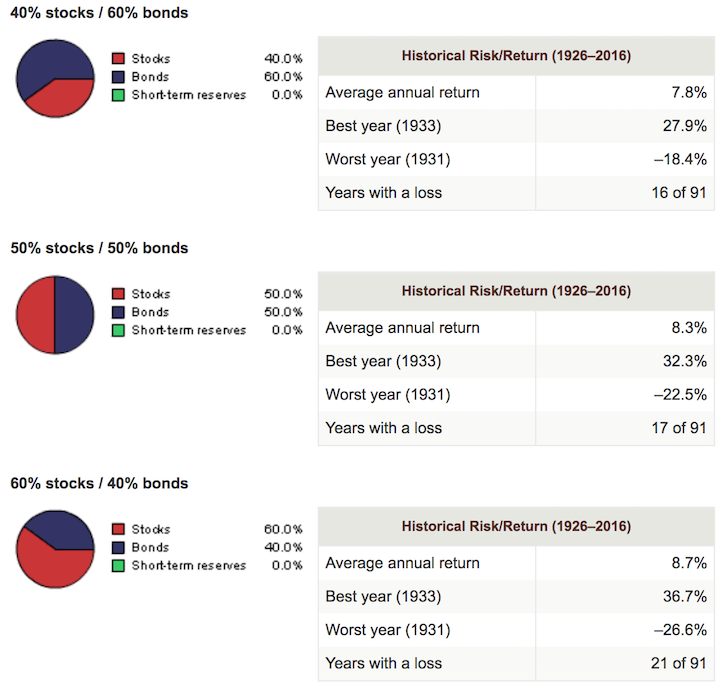

For most retirees, allocating at most 60% of their funds in stocks is a good limit to consider. An average annual return of 8.7% is more than 4X the rate of inflation and 3.3X the risk free rate of return. But you’ve got to ask yourself how comfortable you’ll feel losing over 20% of your money during a serious downturn. If you’re over 65 years old with no other sources of income, you will likely be sweating some bullets.

For the first two years after leaving work, my public investment portfolio was around 60% stocks / 40% bonds. Once I got out of early retirement mode by working on my online business, I got more aggressive in stocks because my business income began to surpass my investment income.

Related: Ranking The Best Passive Income Investments

Source: Vanguard

Growth Based Portfolio

To be comprehensive, let’s take a look at the risk / reward metrics for portfolios with 70% – 100% allocations in stocks. These portfolio allocations are mostly for those who are looking to build a retirement nest egg you’ve already built.

Even with a 100% allocation in stocks, the average annual return is only 10.2%. But there have been 25 years of losses out of 91 years, and in the worst year you would have lost 43% of your money. Losing 43% of your money is fine if you are 30 years old with 20+ years of work left in you. But not so much if your goal is to spend the rest of your days cruising around the world.

Unless you retired before the age of 50, have a variety of passive income streams, run a lifestyle business, or have a net worth equal to over 30X your annual expenses in retirement, I wouldn’t have greater than a 70% allocation to stocks.

Related: Target Net Worth Amounts By Age Or Work Experience For Financial Freedom Seekers

Source: Vanguard

Eliminate Financial Worry In Retirement

Now that you know what the risk/reward metrics are for the above portfolio compositions, you can decide on an investment strategy that best suits your needs.

Don’t let money get in the way of a wonderful retirement. Your investments should be a relatively worry-free tailwind that ensures you never have to return to the salt mines again. If you are starting to worry about your risk exposure, then dial down risk by raising more cash or rebalancing more towards bonds.

Yes, it can get annoying if you underperform your respective benchmarks. But you’ve got to remember that you’ve already won the game. Every single dollar you make above the rate of inflation is gravy. During bull markets, you’ll sometimes be able to return a greater amount from your investments than you would make at your job.

The pain of losing money is always much worse than the joy of making money. If you’ve already got all the money you’ll ever need, there simply is no point taking outsized risk.

Related:

The Main Types Of Risk Exposure To Be Aware Of

The Fear Of Running Out Of Money In Early Retirement Is Overblown

https://www.financialsamurai.com/wp-content/uploads/2018/01/How-To-Invest-in-retirement.m4a

The post How Much Investment Risk To Take In Retirement: Various Portfolio Compositions To Consider appeared first on Financial Samurai.

from Financial Samurai https://www.financialsamurai.com/how-much-investment-risk-to-take-in-retirement/